Random Forest Regression

Random Forest Regression is a powerful machine learning algorithm used for predictive analytics. It constructs multiple decision trees and averages their output...

3 min read

Machine Learning

Regression

+3

Monte Carlo Methods are computational algorithms using repeated random sampling to solve complex, often deterministic problems. Widely used in finance, engineering, AI, and more, they allow modeling of uncertainty, optimization, and risk assessment by simulating numerous scenarios and analyzing probabilistic outcomes.

Monte Carlo Methods use random sampling to solve complex problems, aiding fields like finance, engineering, and AI. They model uncertainty, optimize decisions, and assess risks but require significant computational power and quality random numbers.

Monte Carlo Methods, also referred to as Monte Carlo experiments, are a class of computational algorithms that rely on repeated random sampling to obtain numerical solutions to complex problems. The fundamental principle of Monte Carlo Methods is harnessing randomness to solve problems that might be deterministic in nature. The method is named after the Monte Carlo Casino in Monaco, reflecting the element of chance central to these techniques. This concept was pioneered by mathematician Stanislaw Ulam, who was inspired by the stochastic nature of gambling. Monte Carlo Methods are critical in fields requiring optimization, numerical integration, and sampling from probability distributions.

Monte Carlo Methods are widely used in various domains such as physics, finance, engineering, and artificial intelligence (AI), especially where they assist in decision-making processes under uncertainty. The flexibility of Monte Carlo simulations to model phenomena with uncertain variables makes them invaluable for risk assessment and probability forecasting.

The genesis of Monte Carlo Methods dates back to the 1940s, during the development of nuclear weapons under the Manhattan Project. Ulam and John von Neumann utilized these methods to solve complex integrals related to neutron diffusion. The approach quickly gained traction across various scientific disciplines due to its versatility and effectiveness in dealing with problems involving randomness and uncertainty.

At the heart of Monte Carlo Methods is the process of random sampling. This involves generating random numbers to simulate different scenarios and assess potential outcomes. The reliability of Monte Carlo results is heavily dependent on the quality of these random numbers, which are typically produced using pseudorandom number generators. These generators offer a balance of speed and efficiency compared to traditional random number tables. The robustness of results can be significantly improved by employing techniques such as variance reduction and quasi-random sequences.

Monte Carlo simulations leverage probability distributions to model the behavior of variables. Common distributions include the normal distribution, characterized by its bell-shaped, symmetric curve, and the uniform distribution, where all outcomes are equally likely. The selection of an appropriate distribution is crucial as it affects the simulation’s accuracy and applicability to real-world scenarios. Advanced applications might use distributions like the Poisson or exponential distributions to model specific types of random processes.

In Monte Carlo simulations, input variables, often treated as random variables, are the independent variables that influence the system’s behavior. Output variables are the results of the simulation, representing potential outcomes based on the inputs. These variables can be continuous or discrete and are essential for defining the model’s scope and constraints. Sensitivity analysis is often conducted to determine the impact of each input variable on the outputs, guiding model refinement and validation.

Standard deviation and variance are critical statistical measures in understanding the spread and reliability of simulation results. Standard deviation provides insights into the variability from the mean, while variance measures the degree of spread within a set of values. These metrics are crucial for interpreting simulation results, particularly in assessing the risk and uncertainty associated with different outcomes.

Monte Carlo simulations follow a structured methodology:

Advanced Monte Carlo simulations might incorporate techniques such as Markov Chain Monte Carlo (MCMC), which is particularly useful for sampling from complex probability distributions. MCMC methods are employed in Bayesian statistics and machine learning, where they aid in approximating posterior distributions for model parameters.

Start your free trial today and see results within days.

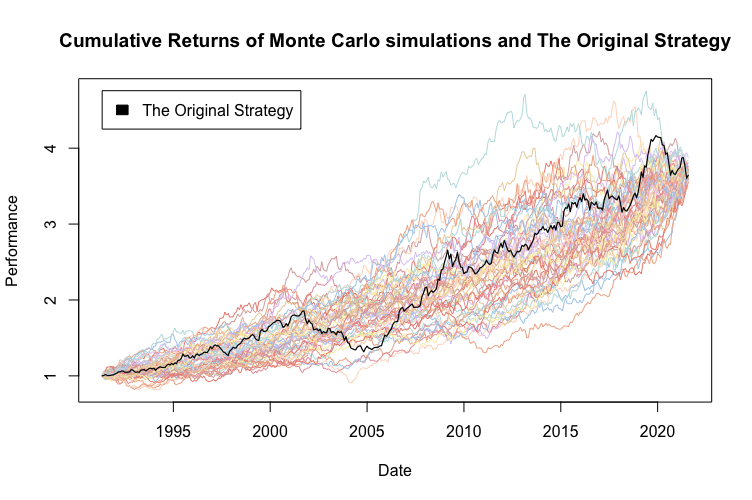

Monte Carlo simulations are indispensable in financial modeling, used to estimate the probability of investment returns, assess portfolio risks, and price derivatives. By simulating thousands of market scenarios, financial analysts can predict potential gains or losses and develop strategies to mitigate risks. This approach is crucial for stress testing financial models and evaluating the impact of market volatility on investment portfolios.

In engineering, Monte Carlo methods simulate the reliability and performance of systems under varying conditions. For instance, they can predict the failure rates of components in mechanical systems, ensuring products meet safety and durability standards. These simulations are also applied in quality control and process optimization, where they help identify potential defects and inefficiencies.

In AI, Monte Carlo methods enhance decision-making algorithms, especially in environments with high uncertainty. These methods help AI systems evaluate the potential outcomes of different actions, improving their ability to predict and adapt to changes. Monte Carlo Tree Search (MCTS) is a notable application in game playing and decision-making tasks, where it enables AI to make informed decisions even with incomplete information.

Project managers use Monte Carlo simulations to forecast project timelines and budgets, accounting for uncertainties like delays and cost overruns. This approach helps in planning and resource allocation by providing probabilistic estimates of project completion. Monte Carlo methods are particularly useful in risk management, where they help identify and quantify potential risks affecting project objectives.

Environmental scientists apply Monte Carlo simulations to model complex ecological systems and predict the impact of changes in environmental variables. This is crucial for assessing risks and developing effective conservation strategies. Monte Carlo methods are used in climate modeling, biodiversity assessment, and environmental impact studies, providing insights into the potential consequences of human activities on natural ecosystems.

While Monte Carlo Methods offer significant advantages, they also present challenges:

Get latest tips, trends, and deals for free.

In the realm of artificial intelligence, Monte Carlo Methods are integral to developing intelligent systems capable of reasoning under uncertainty. These methods complement machine learning by providing probabilistic frameworks that enhance the robustness and adaptability of AI models.

For instance, Monte Carlo Tree Search (MCTS) is a popular algorithm in AI, especially in game playing and decision-making tasks. MCTS uses random sampling to evaluate potential moves in a game, enabling AI to make informed decisions even with incomplete information. This technique has been instrumental in the development of AI systems that can play complex games like Go and chess.

Furthermore, the integration of Monte Carlo simulations with AI technologies like deep learning and reinforcement learning opens new avenues for building intelligent systems that can interpret vast amounts of data, recognize patterns, and predict future trends with greater accuracy. These synergies enhance the capability of AI models to learn from uncertain data and improve their decision-making processes in dynamic environments.

Monte Carlo Methods are a powerful set of computational algorithms used for simulating and understanding complex systems. These methods rely on repeated random sampling to obtain numerical results and are widely employed in fields such as physics, finance, and engineering. Below are some significant scientific papers that delve into various aspects of Monte Carlo Methods:

Fast Orthogonal Transforms for Multi-level Quasi-Monte Carlo Integration

Authors: Christian Irrgeher, Gunther Leobacher

This paper discusses a method for combining fast orthogonal transforms with quasi-Monte Carlo integration, improving the efficiency of the latter. The authors demonstrate that this combination can significantly enhance the computational performance of multi-level Monte Carlo methods. The study provides examples to validate the improved efficiency, making it a valuable contribution to computational mathematics. Read more

The Derivation of Particle Monte Carlo Methods for Plasma Modeling from Transport Equations

Author: Savino Longo

This research provides a detailed analysis of deriving Particle and Monte Carlo methods from transport equations, specifically for plasma simulation. It covers techniques like Particle in Cell (PIC) and Monte Carlo (MC), offering insights into the mathematical foundation of these simulation methods. The paper is crucial for understanding the application of Monte Carlo methods in plasma physics. Read more

Projected Multilevel Monte Carlo Method for PDE with Random Input Data

Authors: Myoungnyoun Kim, Imbo Sim

The authors introduce a projected multilevel Monte Carlo method aimed at reducing computational complexity while maintaining error convergence rates. The study highlights that multilevel Monte Carlo methods can achieve desired accuracy with less computational time compared to traditional Monte Carlo methods. Numerical experiments are provided to substantiate their theoretical claims. Read more

Inference with Hamiltonian Sequential Monte Carlo Simulators

Author: Remi Daviet

This paper proposes a novel Monte Carlo simulator combining the strengths of Sequential Monte Carlo and Hamiltonian Monte Carlo simulators. It is particularly effective for inference in complex and multimodal scenarios. The paper includes several examples demonstrating the robustness of the method in dealing with difficult likelihoods and target functions. Read more

Antithetic Riemannian Manifold and Quantum-Inspired Hamiltonian Monte Carlo

Authors: Wilson Tsakane Mongwe, Rendani Mbuvha, Tshilidzi Marwala

The research presents new algorithms that enhance Hamiltonian Monte Carlo methods by incorporating antithetic sampling and quantum-inspired techniques. These innovations improve sample rates and reduce variance in estimations. The study applies these methods to financial market data and Bayesian logistic regression, demonstrating significant improvements in sampling efficiency. Read more

Monte Carlo Methods are a class of computational algorithms that use repeated random sampling to obtain numerical solutions to complex problems, often involving uncertainty and probabilistic modeling.

They are widely used in finance for risk analysis and portfolio optimization, in engineering for reliability and quality control, in AI for decision-making under uncertainty, and in project management and environmental science for forecasting and risk assessment.

The main advantage is their ability to model uncertainty and simulate a wide range of possible outcomes, providing valuable insights for decision-making in complex systems.

Monte Carlo Methods can be computationally intensive, require high-quality random number generation, and may face challenges like the curse of dimensionality as model complexity increases.

Explore how Monte Carlo Methods and AI-driven tools can enhance decision-making, risk analysis, and complex simulations for your business or research.

Random Forest Regression is a powerful machine learning algorithm used for predictive analytics. It constructs multiple decision trees and averages their output...

Boosting is a machine learning technique that combines the predictions of multiple weak learners to create a strong learner, improving accuracy and handling com...

A deterministic model is a mathematical or computational model that produces a single, definitive output for a given set of input conditions, offering predictab...

Cookie Consent

We use cookies to enhance your browsing experience and analyze our traffic. See our privacy policy.